This guide was updated in July 2026.

If you’re responsible for energy budgets, you’ll know that the wholesale price of electricity is only part of the story. Typically, 60 – 65% of your electricity bill is made up of non-commodity costs – network charges and green levies that sit outside your contracted unit rate.

2026 so far has seen an overall rise in non-commodity charges, largely to modernise grid infrastructure and develop new renewable generation capacity. We expect these charges to remain high in 2027. To help you plan your energy budget, we’ve put together a breakdown of non-commodity cost changes for electricity in 2026 and 2027.

For a wider understanding of non-commodity costs, download our new Non-Commodity Cost Guide. We explain the different types of non-commodity costs, what they are for, and importantly, what you can do to reduce the impact on your energy bills.

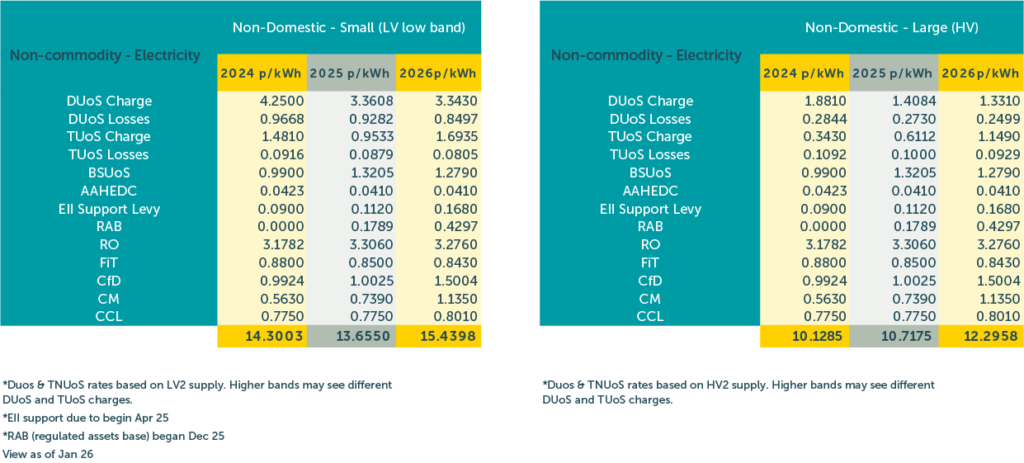

A snapshot of non-commodity prices

This table shows non-commodity prices for electricity in 2024, 2025 and 2026, showing fluctuations across all the charges:

Electricity non-commodity price changes: a breakdown

TNUoS: sharp increase from 2026 onwards

We are set to see a sharp increase in transmission network costs, to fund the large amount of transmission system upgrades and projects due over the next 5 years.

- April 2026-27: There will be an increase of up to 102% compared to April 2025 rates

- Rates until 2031: Much higher than previously forecast.

DUoS: stable but expect steep rises in 2027

DUoS are the charges for using the local electricity network, set by your regional Distribution Network Operator (DNO).

From April 2026:

- Standing charges are down 6% on average. Low Voltage (LV) sites will see larger reductions than High Voltage (HV) sites.

- Maximum Import Capacity (MIC) charges are up 5%on average.

- Red band charges (peak-time electricity rates) are (on average) up 1% for LV sites, up 4% for LVS sites (Low Voltage Substation), but down 7% on average for HV sites.

From April 2027:

- We see steep DUoS rises. Charges were relatively flat in 2025/2026 because DNOs had previously over-recovered revenue. With those monies now repaid, they will raise charges to fund infrastructure investment and rising operating costs.

- Standing charges increase between 65% and 77%

- Red band charges increase (up to 28% on HV).

- MIC charges increase – averaging around 0.77p/kVA/day higher than April 2026 charges.

BSUoS (Balancing Services Use of System): uncertainty, likely rises

Balancing services are vital for maintaining a perfect balance between the electricity going into the grid and the electricity being used. If the balance is wrong, the grid will operate at the wrong frequency, which could cause blackouts and costly damage to infrastructure.

- Fixed seasonal tariffs: BSUoS charges are set in advance for the periods April – September and October – March.

- Three months’ notice: As of April 2026, each seasonal tariff is published three months in advance (previously nine months)

- Current pricing: BSUoS charges for the current period (Tariff 7, April to September 2026) are £13.74/MWh.

- From October 2026: The next period, Tariff 8, runs from October 2026 to March 2027. Tariff 8 was originally set at £12.49/MWh but the operator is now reconsidering.

Operator NESO can’t perfectly predict BSUoS costs, so the tariff for each six-month season is designed to collect any overcharging or undercharging from the previous one. However, costs in the first part of 2026 have been higher than predicted and NESO is now considering the unusual move of adjusting Tariff 8 upwards even though it’s already been set.

The Iran conflict has made global energy prices more volatile, which makes the balance between supply and demand less predictable, creating a need for more frequent balancing interventions. The same volatility makes some of these interventions very expensive.

The shift to renewables means cheaper energy overall, but also creates a greater need for balancing services because renewable output is less predictable and controllable.

Contracts for Difference (CfD): stable until 2027

The CFD funds new low-carbon generation projects in the UK.

- The latest CfD forecasts reduce for most forward cases, with Q1 2026 interim levy around £10/MWh, similar to the past two quarters.

- Forward cases out to Q3 2027 are stable for now, however, Q3 2027 may see a rise to £20.67/MWh when the Drax biomass project joins the scheme.

Feed in Tariff (FiT): stable

- FiT remains steady. It remains in the 0.7-0.9p/kWh region, with reconciliations applied by most suppliers.

- Summer 2025 saw an uplift from some suppliers due to the brighter weather and lower net demand – if Summer 2026 sees similar weather, FiT will likely see more seasonal pricing.

Capacity Market (CM): increasing

- CM levels are projected to increase, expecting to breach £10/MWh (smeared unit cost) in winter 2025 – 2026, with auction figures remaining high for future years. The next auction is T-1 for winter of 2026 – 2027.

- T-4 for winter 2029 – 2030, is scheduled to be announced for March 2026.

AAHEDC: stable

- AAHEDC subsidises electricity distribution costs in specific, sparse areas, primarily the North of Scotland.

- It will remain in line with prior years, with a small decrease from April 2026

- The usual cost is around 0.042p/kWh.

Climate Change Levy (CCL): increasing

- Increasing from April 26 to 0.801p/kWh (from 0.775p/kWh) and again in Apr 27 to 0.827p/kWh for both electricity and gas.

Many of these charges (e.g. CFD, CM and FiT) are only known and published after the period that they cover and therefore pass-through contracts will get reconciliations (these can sometimes be over a year later).

New non-commodity charges

Three new levies have been introduced in recent years, to boost industrial competitiveness and fund nuclear and hydrogen production.

EII Support Levy (Network Charging Compensation Scheme)

- This levy on regular business consumers funds discounts for energy intensive industries.

- April 2025 saw suppliers billing from around £0.7-1.4/MWh.

- April 2026 sees an increase of 50%, as support for EIIs increases.

Regulated Assets Base Levy (RAB)

- This new charge is to help fund nuclear infrastructure.

- The interim rate is £3.49/MWh plus a small operational fee

- The next 2 years of quarterly price projections are relatively stable, around £3.50-4.50/MWh.

Non-commodity cost trends 2026-27

Cost component | Trend | What to watch |

TNUoS (transmission network costs) |

| Major increase – up to 102% rise in 2026 and 2027 |

DUoS (local network costs) |

| Stable in 2026 but expect a huge spike in 2027. |

BSUoS (grid balanding costs) |

| Expect a higher rate October 2026–March 2027 |

Renewable Obligation |

| Slight decrease, linked to CPI inflation |

Contracts for Difference |

| Rise expected in Q3 2027 |

Feed in Tariff |

| We may see a seasonal uplift in Summer 2026 |

Capacity Market |

| Likely to remain high for future years |

AAHEDC |

| |

Climate Change Levy |

| Increasing in April 2026 and again in 2027 |

EII Support Levy |

| Increasing by 50% in April 2026 |

RAB Levy |

| Implemented November 2025 |

Increasing

Increasing

Stable

StableHow to reduce your non-commodity costs

The bottom line is that non-commodity costs are increasing.

While a few elements have reduced or stabilised in the short term, the wider trend is upward, driven largely by the need to fund long-term grid infrastructure upgrades and low-carbon technologies.

For most businesses, this means non-commodity costs will continue to take up a growing share of total energy spend over the next few years.

The good news is that businesses are not powerless. There are practical ways to reduce exposure and protect budgets — whether through reviewing how and when energy is used, reassessing capacity levels, or making use of available schemes and procurement structures.

We’ve brought all of this together in our new Non-Commodity Cost Guide. It explains what each charge is, and importantly, how you can reduce your exposure to increasing costs.

Download our Non-Commodity Cost Guide to learn more. Or, get in touch with one of the experts at Sustainable Energy First via the form below.

")

")

: the UK’s renewable energy support scheme explained")

")