SECR: What’s the difference between reporting requirements for quoted and unquoted companies?

Streamlined Energy and Carbon Reporting (SECR) requirements cover quoted companies, large unquoted companies and large Limited Liability Partnerships (LLPS) – but the rules are different depending on your type of company.

Here we break down the main differences.

Quoted companies

Quoted companies have already been reporting on GHG emissions since 2013, as part of Mandatory GHG Reporting. Under SECR, energy use and energy efficiency measures must also now also be included.

Quoted companies are now required to report on:

- ALL greenhouse gas (GHG) emissions from activities they are responsible for – globally. That includes carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF6). While it’s not a legal requirement, you should consider reporting on nitrogen trifluoride NF3, especially if material to your operations.

- This is important – because although the bulk of your emissions is likely to be carbon dioxide (from the use of electricity, gas and transport), other greenhouse gas gases are, like-for-like, much more potent. For example, one tonne of nitrous oxide, emitted from fertiliser, has the same global warming impact as 298 tonnes (or has 300x the warming power) of carbon dioxide.

- You must also report on the underlying global energy use that was used to calculate your GHG emissions.

Large unquoted companies and large LLPs are required to report on:

- UK ONLY energy use (as a minimum gas, electricity and transport, including UK offshore area), and the associated greenhouse emissions.

- You are not required to report on ALL greenhouse gas emissions, just those associated with your UK energy use.

The government’s SECR guidance breaks down the difference:

| Quoted companies | Large unquoted companies and LLPs |

| Annual GHG emissions from activities for which the company is responsible including combustion of fuel and operation of any facility; and the annual emissions from the purchase of electricity, heat, steam or cooling by the company for its own use | UK energy use (as a minimum gas, electricity and transport, including UK offshore area) |

| Underlying global energy use | Associated greenhouse gas emissions |

| Previous year’s figures for energy use and GHG | Previous year’s figures for energy use and GHG emissions |

| At least one intensity ratio | At least one intensity ratio |

| Energy efficiency action taken | Energy efficiency action taken |

| Methodology used | Methodology used |

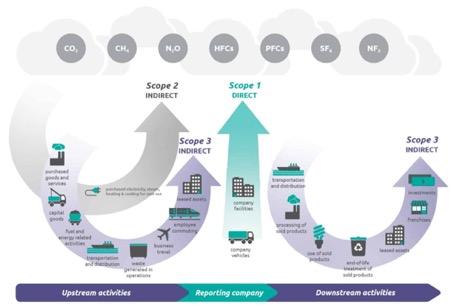

A quick explainer on “Scopes of Emissions”

Best practice for identifying and organising all your different emissions-releasing business activities is to put them into three groups known as scopes. Only two of the three scopes are compulsory to report under SECR.

- Scope 1 emissions (Direct) is the company’s direct emissions. They come from sources owned or controlled by the company, like gas emissions from furnaces, methane emissions from agriculture, fuel burned by company vehicles and so on.

- Scope 2 emissions (Indirect) are those generated as a result of the energy you purchase from suppliers. For example, a retail chain might be paying energy suppliers to heat and light its shops. The associated emissions are considered “indirect” because they happen as a direct result of your company’s activities, but you don’t own or control the energy source.

- Scope 3 emissions (Other Indirect) are also indirect. They are also known as “value chain emissions” or “supply chain emissions” because they are generated by sources connected to a business rather than by the business itself. (This could include customers and waste disposal services as well as suppliers and distributors.)

Only ONE type of Scope 3 emissions is compulsory to report under SECR, and it’s only compulsory for large unquoted companies and large LLPs: that is, the fuel burned during business-related travel if the vehicle involved is a rental or belongs to an employee who buys the fuel.

Going further

Increasing numbers of businesses in scope of SECR are going beyond the legal minimum and reporting their Scope 3 emissions as well as Scopes 1 and 2. There are many tangible business benefits to reporting on your Scope 3 emissions, especially if your business is serious about reducing its greenhouse gas emissions and demonstrating it is a responsible business as part of any other reporting schemes, whether they be voluntary or compulsory or for public relations. Check out our Scope 3 emissions FAQ for a quick introduction.

However, it is crucial to get the legally mandated basics right first, and many companies find that this is enough of a challenge in their first year of SECR reporting. This is one area where getting expert advice early on could remove a lot of potential problems in future. BiU’s Energy Advice Experts have extensive experience of guiding companies through their SECR compliance, and are always happy to answer questions. Get in touch if you’d like to know more. You can also download our SECR guide or check out our SECR FAQs.

")

: the UK’s renewable energy support scheme explained")

")